Guide to mortgage rates

There are many different types of mortgage rates available and these are some of the options.

If you would like some friendly, straightforward mortgage advice from our partners Embrace Financial Services, then call free on 0800 056 4508^ or book an appointment.

^ Calls may be recorded and/or monitored for training and/or data protection purposes.

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Your initial mortgage appointment is without obligation. Embrace Financial Services normally charge a fee for their services; however, it is payable only on the submission of your mortgage application. The fee will depend on your circumstances but the standard fee is £599. Complex cases usually attract a higher fee. Embrace Financial Services will discuss and agree the fee with you prior to submitting any mortgage application.

How a Standard Variable Rate mortgage works

Standard Variable Mortgage.

This is the normal rate charged by the lender without any discounts or special deals. It can be changed by the lender in line with market conditions. This is usually the interest rate that a lender will revert to once the initial deal has finished.

Advantages:

Often no early repayment charges or arrangement fee.

Disadvantages:

Often higher rate than fixed / tracker / discounted mortgages.

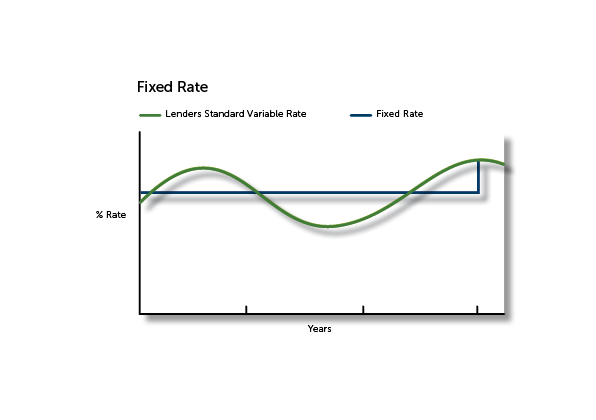

How a Fixed Rate mortgage works

Fixed Rate Mortgage.

The interest rate is fixed for a period of time. After this initial period it reverts to the lender's Standard Variable Rate.

Advantages:

Ability to budget - you know what you will be paying each month for the initial period.

Disadvantages:

Fixed only for an initial period not the whole mortgage term. If interest rates fall you could end up paying more than necessary. An arrangement fee may apply and an early repayment charge may be applied if the loan is redeemed before a specified date.

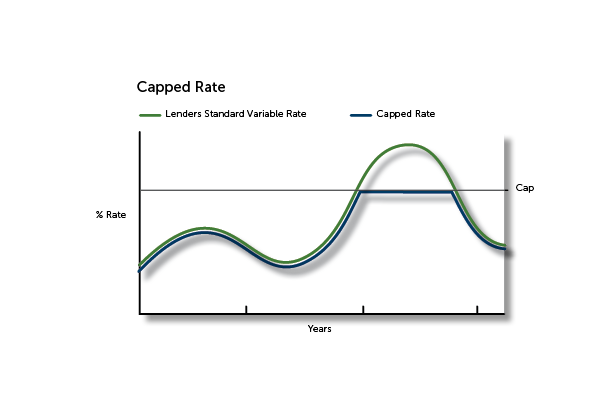

How a Capped Rate mortgage works

Capped Rate Mortgage.

Follows the lender's Standard Variable Rate but there is a maximum interest rate you have to pay. If the mortgage has a cap and a collar then the cap is the maximum interest rate, and the collar is the minimum interest rate.

Advantages:

If rates go up you only have to pay up to the 'ceiling' interest rate.

Disadvantages:

Tend to be more expensive than Fixed or Tracker Mortgages.

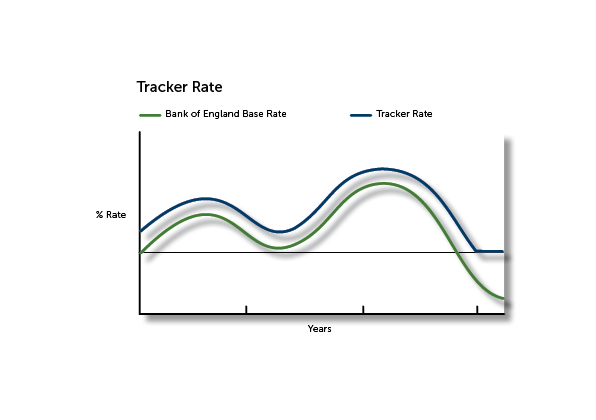

How a Tracker Rate mortgage works

Tracker Rate Mortgage.

The interest rate on your mortgage moves up and down with a particular base rate, such as the Bank of England base rate.

Advantages:

When the index (for example the Bank of England base rate) falls, so will your monthly payment.

Disadvantages:

If the Bank of England rate goes up, so do your monthly payments. Often a minimum % is specified. An arrangement fee may apply and an early repayment charge may be applied if the loan is redeemed before a specified date. Less easy to budget for than with a fixed rate mortgage.

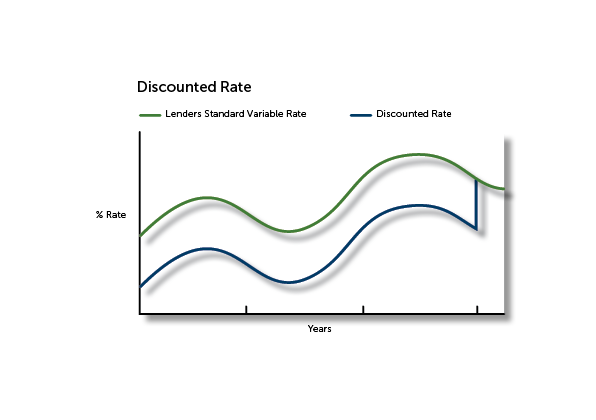

How a Discounted Rate mortgage works

Discounted Rate Mortgage.

With a Discounted Rate Mortgage the mortgage interest rate is reduced by a specified amount for a set period. After this set period, the mortgage reverts to the lender's Standard Variable rate.

Advantages:

When the lender's Standard Variable Rate falls so do your monthly payments and it can provide lower monthly mortgage payments at the start of the mortgage.

Disadvantages:

An arrangement fee may apply and an early repayment charge may be applied if the loan is redeemed before a specified date. Less easy to budget than with a fixed rate mortgage. When the lender's standard variable rate rises so do your monthly payments.

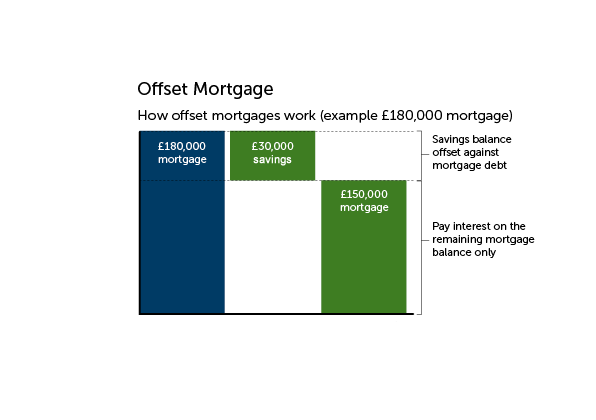

How an Offset mortgage works

Offset Mortgage.

An offset mortgage links your savings or your current account to your mortgage. Interest is calculated on the difference between savings and the mortgage rather than the whole mortgage amount.

Advantages:

- Interest only charged on mortgage balance outstanding once savings balance deducted.

Disadvantages:

- Interest rates can be higher than equivalent non offset products.